Argentina

Argentina Bolivia

Bolivia Brazil

Brazil Chile

Chile Colombia

Colombia Ecuador

Ecuador Paraguay

Paraguay Peru

Peru Uruguay

Uruguay Belize

Belize Costa rica

Costa rica El salvador

El salvador Guatemala

Guatemala Mexico

Mexico Nicaragua

Nicaragua Panama

Panama Dominican Republic

Dominican Republic EN

EN ES

ES

What is your Tax ID in Mexico? – RFC number

Everything you need to know about your company Tax ID (RFC number)! What is the RFC number and what is its purpose? The RFC number is an essential part of the company formation in Mexico.

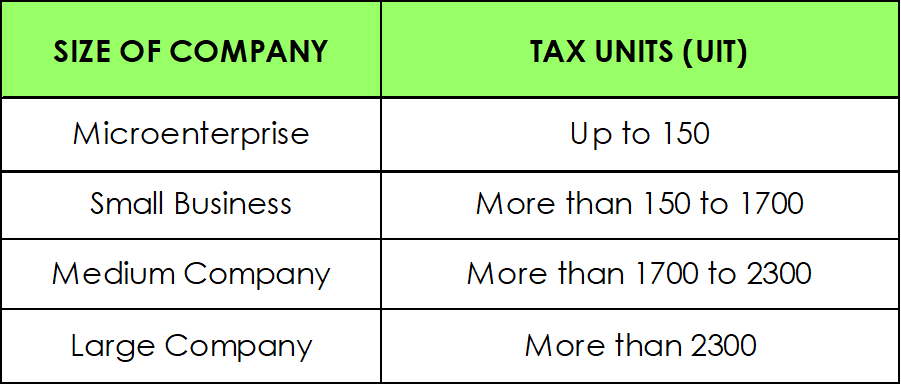

When starting your company in Peru, you must also know the tax and accounting requirements that apply. In this article, we will give general information about such requirements as well as the factors to be considered for good business management, since the type of business and size of the company constituted also influences the payment of taxes.

The Peruvian government classifies companies according to their annual sales revenue in UIT (Tax Unit). It should also be noted that smaller companies pay lower tax rates than large companies.

Source: Ministry of Economy and Finance

The ITU is a taxing unit and it is determined annually by the Ministry of Economy and Finance of Peru, the value of this year (2021) corresponds to PEN 4,400.00.

It is regulated by norms, principles, and institutions that establish the application of taxes based on Legislative Decree N° 771 and it was named Ley Marco del Sistema Tributario Nacional (Legal Framework for Taxation). Here are considered the taxes, contributions, and rates that exist in Peru.

It is enforced by the National Superintendence of Tax Administration – SUNAT nationwide.

Here we will mention some taxes that companies must pay:

It applies to resident and non-resident entities that have a permanent establishment in Peru. Those resident entities pay a rate of 29.5% on their net taxable income and those non-resident entities pay a rate of 30% on income from Peruvian sources.

This tax includes the company’s net income, taxable income, and capital gains. In addition, here you can present commercial expenses that can be deducted from the income. It is important to note that these expenses presented must be directly related to the business activity.

Note: The foreign dividends that a Peruvian entity may receive must be considered in the tax base, which indicates that they are subject to the corporate tax whose rate is 29.5%, in addition to considering that a tax credit is generated because of the foreign tax paid on such dividends.

This tax allows levying the added value of all the transactions made by the companies in all the phases of the production and distribution cycle. It is considered in the purchase and sale of goods, services, construction contracts, sale of real estate, and others.

This tax is aimed to be assumed by the final consumer. It is composed of a 16% rate that corresponds to the taxation of the product/service plus a 2% rate of the Municipal Promotion Tax, which gives a total of 18%.

Note: This tax is known in Peru as Impuesto General a las Ventas – IGV.

All companies are required to declare income and expenses on a monthly and annual basis. A company’s fiscal year is its accounting year, which ends on December 31st. Companies must also file their annual tax return and pay the final tax within a period of three months after the end of the fiscal year. In the mining industry, it should be considered the payment of royalties between 1% and 12% which is calculated based on the gross sale corresponding to the transfer of mineral resources.

If the company does not present its tax returns on time or does not pay the corresponding contributions, the company is subject to fines and/or sanctions that must be paid to SUNAT.

There are contributions that must be paid to the employees on your company’s payroll, such as health and pension fund contributions.

• Health system: The Peruvian health system is divided between the public and private sectors. Generally, employers are required to pay a monthly contribution equivalent to 9% of the employee’s salary.

It should be noted that the employee may be registered in the National Health System where they are treated by EsSalud and the percentage corresponds to 9%, or they may be registered in the Private Health System (EPS) whose rate will depend on the working conditions and the option of the employee.

• Pension fund: There is also a public and private system. However, in this case, the amount is deducted from the employee’s salary and is a rate of approximately 13% for the public pension system, which is headed by the ONP. In the case of the private pension system, headed by the AFPs, the percentage may vary depending on which one is chosen.